The European Language Industry Survey (ELIS) results were published in March 2024, and a lot of the focus at the time was on the negative sentiment and uncertainty that came across. However, the report contains other data and conclusions that have not yet been widely discussed, and ELIA as one of the co-organisers of the survey thought it prudent to raise some of them as conversation topics within the language services industry – and perhaps beyond!

The ELIS survey covers market trends, expectations and concerns, challenges and obstacles, as well as changes in business practices. The questions in the survey were answered by language service companies (LSCs), individual language professionals, training institutes, language service buyers, as well as private and public translation departments.

The first topic we decided to look at is gender in LSC leadership. Here is what Anu Carnegie-Brown and Stéphane Hue saw in the ELIS report and what they had to say on this topic.

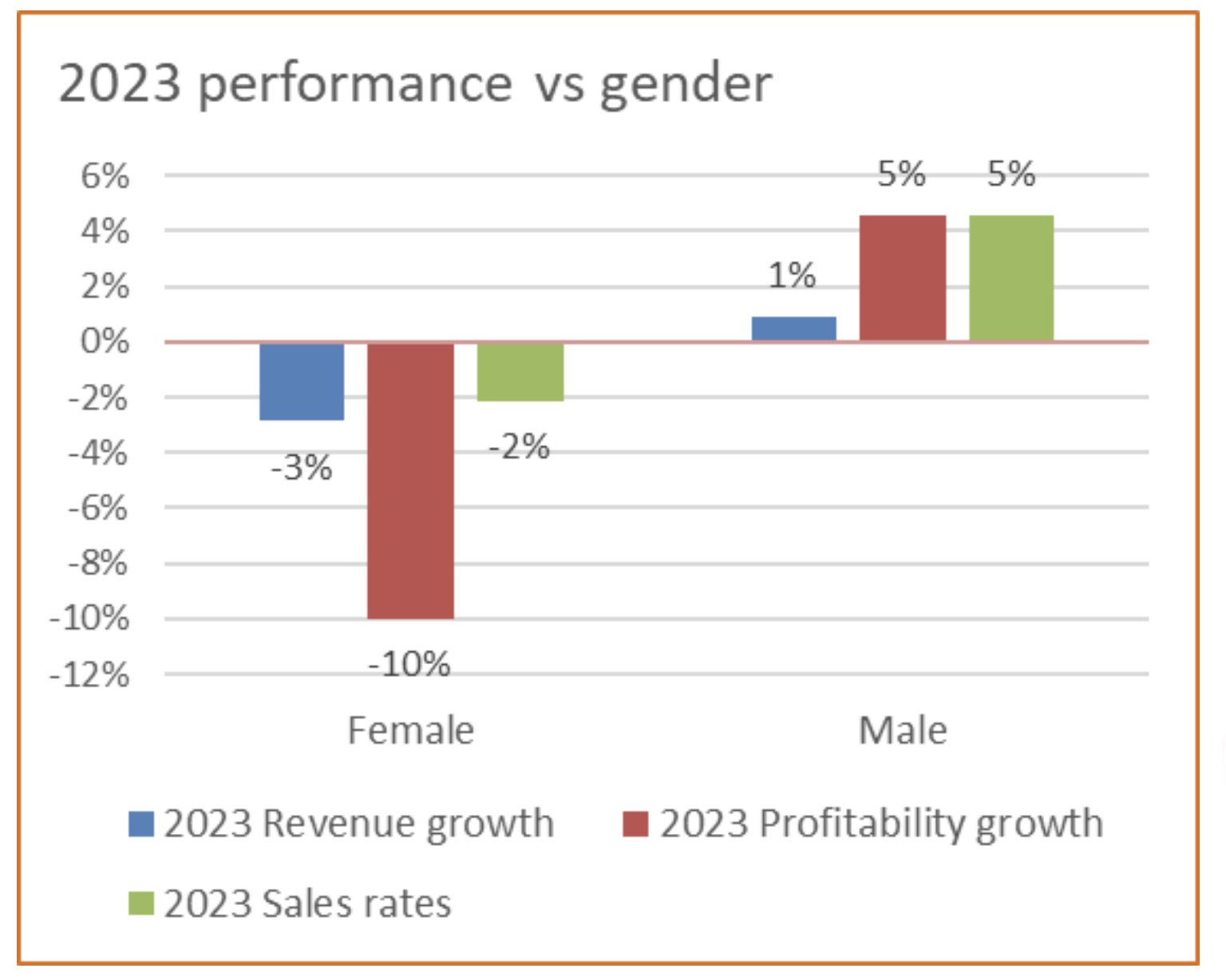

ACB: The ELIS report analyses the results per gender only once, in the context of LSC performance. This in itself is an interesting choice; why not look at the results on any of the other questions per gender? The chart published in the report shows the LSCs’ 2023 performance, with the accompanying text: “The data confirm the gender bias in company performance that was already noticed in the 2023 edition, which is particularly visible in Profitability. The underlying cause is unclear (despite the bias in sales rate evolution), since profit margins, FTE figures and other parameters do not show such bias.”

I picked on this detail in the report because it says that female-led companies didn’t grow last year, in terms of revenue or profit, whereas male-led did. It implies that male LSC CEOs are better growth leaders than female ones, and it mentions that the ‘underlying cause is unclear’. I think it’s important to consider what’s behind this data before settling on any rash conclusion.

ACB: Are the female-led LSCs in this sample also smaller in size than the male-led ones?

The Nimdzi 2024 report states that only 13 of the 100 largest LSCs in the world had a female CEO in 2023. The same report shows that the combined revenue growth in these 100 largest LSCs was 5%. The size of the company may have a more direct correlation to its ability to generate growth in the current market climate than the gender of its CEO.

SH: Can LSCs really be different in this respect from other companies?

The ELIS result contradicts other surveys that are not focused on the language industry. While some could suggest that male psychological behaviour is at stake, a number of academic studies on gender diversity point to the fact that companies with more women in a senior position “are more profitable, more socially responsible, and provide safer, higher-quality customer experiences — among many other benefits” (Harvard Business Review April 2021).

ACB: Should a company’s revenue and profit performance be contributed to one person alone?

Perhaps in an SME of 5-10 people, the leadership team consists of the owner-manager alone, in which case any successful growth strategy and its execution can be entirely attributed to them. But in other companies, surely decisions on how much is invested in growth are taken by the board of directors and the strategies are executed by the whole leadership team.

SH: Might women be more honest when sharing data about their company’s performance?

The ELIS survey is based only on answers provided by the respondents. There has been no fact check. So the gender bias might simply apply to the honesty of the answers, not the real facts. Also, the difference is not really statistically representative.

ACB: Might women typically lead lifestyle businesses and men lead build-to-sell companies?

Lifestyle companies are passion-centred, they nurture long-term business prospects and generate enough profit to allow their shareholders a comfortable living. Build-to-sell companies focus on maximising the value of the business within a short time-frame. I’m fairly certain that financial planning and also how the accounts are presented is rather different in each: a lifestyle company may wish to minimise profit and corporation tax, whereas a build-to-sell one aims to show as much profit as possible.

We invite you to share your thoughts on this topic. What do you think about the survey results and the factors influencing LSC performance by gender? Join the conversation on LinkedIn and let’s discuss!